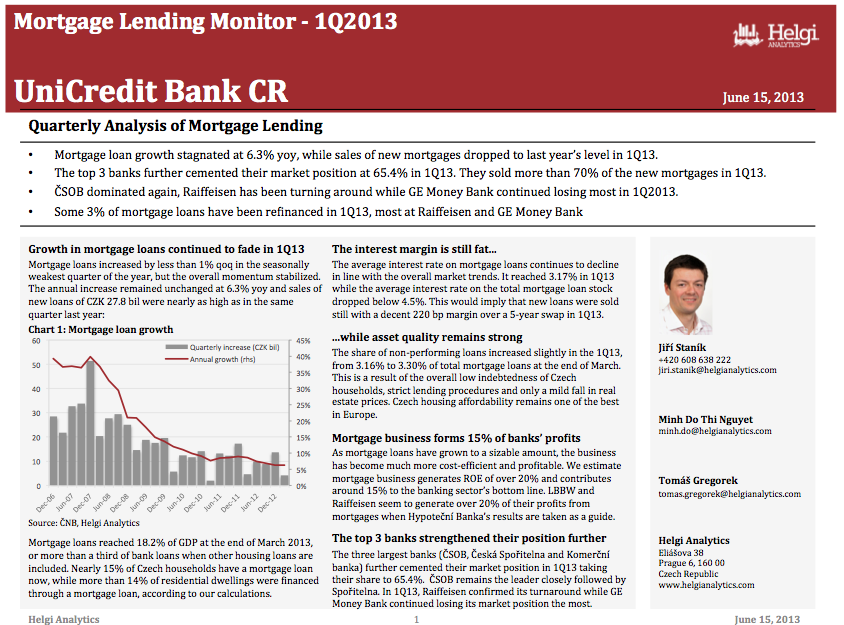

This report analyses the housing lending in the Czech Republic for the 1Q2013. You will find all the necessary details regarding volume growth (for both, the mortgage as well as Building Society lending), market share, margin and asset quality development in the mortgage segment. Also, based on the example of Hypotecni Banka, we calculate profitability of the mortgage busines for each bank.

This report focuses specifically on development in UniCredit Czech Republic in the 1Q2013. The key highlights are:

UniCredit outperforms the market...

UniCredit’s mortgage loans increased by an impressive 3.0% qoq and 17.3% yoy in 1Q13, nearly three times as fast as the overall market. The bank has been expanding its mortgage loan book by 15% a year over the last three years and has been clearly outperforming the market since the end of 2008.

...as well as its closest peers

Following the completion of the triple merger in 2007 (UniCredit/HVB/Živnobanka), UniCredit bank has been increasingly focusing on business, at least when judged by numbers. The bank has increased its market share of mortgage loans from around 3% in 2007 to 4.4% at the end of March 2013.

In terms of new production, the bank sold 7.1% of the new mortgages generated on the market in 2012 and 7.5% in 1Q13.

The bank’s engine seems to have been gradually speeding up and the bank seems to be benefiting from the strategic re-direction of a few market players.

When we look at the new production sold in 2012, UniCredit has been taking over some of the market share from Raiffeisenbank. In 1Q13, GE Money Bank seems to be the main target UniCredit has been going after:

Mortgages – 10-15% of UniCredit’s profit?

Residential mortgage loans represented 16.2% of UniCredit’s total loans at the end of March 2013. That is twice as much in relative terms as of the end of 2007; on the other hand, it is only a half of the level seen at the three largest banks in the country.

This is also significantly less than at UniCredit’s closest peers, Raiffeisenbank (with 35% in March 2013) and GE Money Bank (over 20%). Apart from the mergers, UniCredit’s overall conservative approach towards mortgage lending in CEE and relatively smaller focus on the retail area could be blamed for that.

When Hypoteční banka’s financials are taken as a benchmark (for more details see page 9), we believe mortgage lending business generates around 10-15% of UniCredit’s overall profitability now.

This is less than the 24% of Raiffeisenbank and 20% of ČSOB but roughly in line with the numbers we calculated for Komerční Banka and Česká Spořitelna

Helgi Library

Helgi Library