This report analyses the performance of the Bank for the 3Q2014. You will find all the necessary details regarding volume growth, market share, margin and asset quality development in the Bank.

The key highlights are:

SSČS's profit falls 16.5%...

SSČS reported a net profit of CZK 102 mil. in 3Q2014, down 16.5% yoy compared to the same period last year. Despite the bottom line deterioration, the quarter provides quite a reassuring message - underlying revenue continues growing (net interest income up 14% yoy).

Otherwise, the quarter's profitability was marked by a number of one-off items such as a very high trading profit, an unusual fall in other expenses (the other leg of the trading profit?), or an extraordinarily high cost of risk (in spite of already good provision coverage of bad loans).

...but revenue continues growing...

An ongoing increase in net interest income is the key message of the quarter in our view. The 14% increase is a result of balance sheet re-pricing as both loans as well as deposits continued declining.

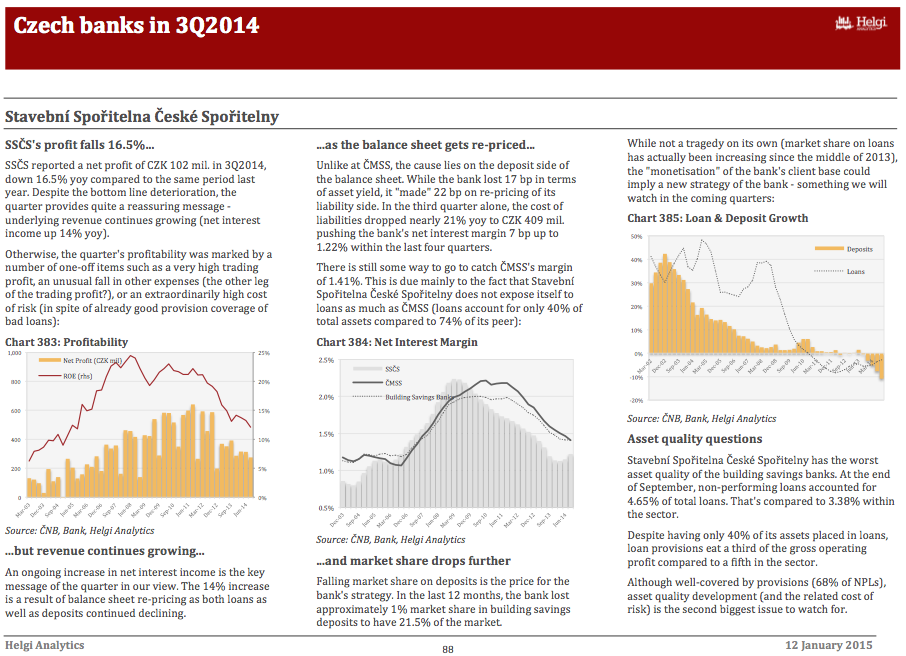

...as the balance sheet gets re-priced...

Unlike at ČMSS, the cause lies on the deposit side of the balance sheet. While the bank lost 17 bp in terms of asset yield, it "made" 22 bp on re-pricing of its liability side. In the third quarter alone, the cost of liabilities dropped nearly 21% yoy to CZK 409 mil. pushing the bank's net interest margin 7 bp up to 1.22% within the last four quarters.

There is still some way to go to catch ČMSS's margin of 1.41%. This is due mainly to the fact that Stavební Spořitelna České Spořitelny does not expose itself to loans as much as ČMSS (loans account for only 40% of total assets compared to 74% of its peer).

...and market share drops further

Falling market share on deposits is the price for the bank's strategy. In the last 12 months, the bank lost approximately 1% market share in building savings deposits to have 21.5% of the market.

While not a tragedy on its own (market share on loans has actually been increasing since the middle of 2013), the "monetisation" of the bank's client base could imply a new strategy of the bank - something we will watch in the coming quarters.

Asset quality questions

Stavební Spořitelna České Spořitelny has the worst asset quality of the building savings banks. At the end of September, non-performing loans accounted for 4.65% of total loans. That's compared to 3.38% within the sector.

Despite having only 40% of its assets placed in loans, loan provisions eat a third of the gross operating profit compared to a fifth in the sector.

Although well-covered by provisions (68% of NPLs), asset quality development (and the related cost of risk) is the second biggest issue to watch for.

You will find more details about the bank at www.helgilibrary.com/companies

Helgi Library

Helgi Library