This report analyses the housing lending in the Czech Republic for the 1Q2013. You will find all the necessary details regarding volume growth (for both, the mortgage as well as Building Society lending), market share, margin and asset quality development in the mortgage segment. Also, based on the example of Hypotecni Banka, we calculate profitability of the mortgage business for each bank.

This report provides a summary of the development in the 1Q2013. The key highlights are:

-

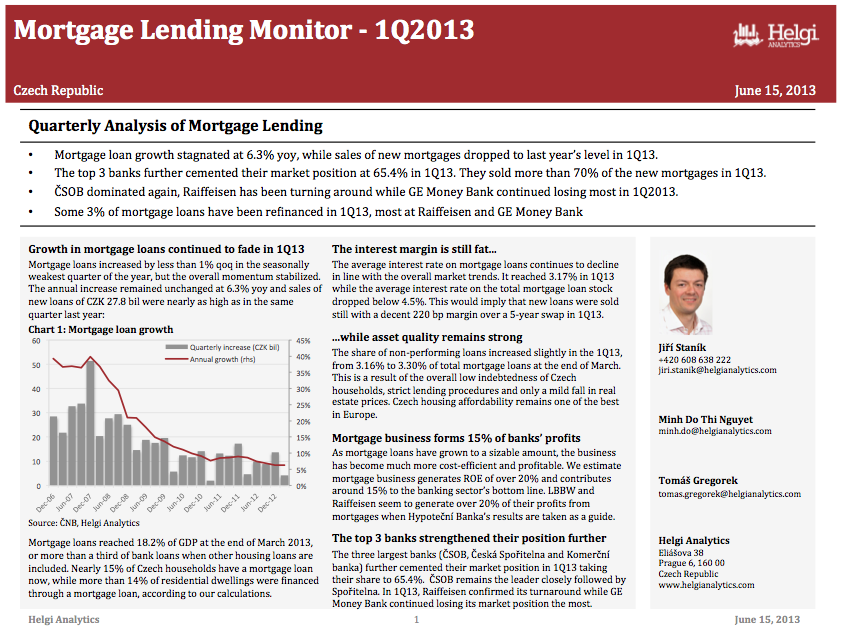

Mortgage loans increased by less than 1% qoq in the seasonally weakest quarter of the year, but the overall momentum stabilized. The annual increase remained unchanged at 6.3% yoy and sales of new loans of CZK 27.8 bil were nearly as high as in the same quarter last year:

-

Mortgage loans reached 18.2% of GDP at the end of March 2013, or more than a third of bank loans when other housing loans are included. Nearly 15% of Czech households have a mortgage loan now, while more than 14% of residential dwellings were financed through a mortgage loan, according to our calculations.

-

The average interest rate on mortgage loans continues to decline in line with the overall market trends. It reached 3.17% in 1Q13 while the average interest rate on the total mortgage loan stock dropped below 4.5%. This would imply that new loans were sold still with a decent 220 bp margin over a 5-year swap in 1Q13.

-

The share of non-performing loans increased slightly in the 1Q13, from 3.16% to 3.30% of total mortgage loans at the end of March. This is a result of the overall low indebtedness of Czech households, strict lending procedures and only a mild fall in real estate prices. Czech housing affordability remains one of the best in Europe.

-

As mortgage loans have grown to a sizable amount, the business has become much more cost-efficient and profitable. We estimate mortgage business generates ROE of over 20% and contributes around 15% to the banking sector’s bottom line. LBBW and Raiffeisen seem to generate over 20% of their profits from mortgages when Hypoteční Banka’s results are taken as a guide.

-

The three largest banks (ČSOB, Česká Spořitelna and Komerční banka) further cemented their market position in 1Q13 taking their share to 65.4%. ČSOB remains the leader closely followed by Spořitelna. In 1Q13, Raiffeisen confirmed its turnaround while GE Money Bank continued losing its market position the most.

Helgi Library

Helgi Library